Resolution

UPDATED 15 August 2022

On 15 March 2020, the Government announced the implementation of emergency measures, administered through the Department of Employment Affairs and Social Protection (DEASP), to enable workers who are temporarily laid off due to the COVID-19 (Coronavirus) pandemic to claim l support payments.

The scheme is open to employees who were on the employer’s payroll as at 29 February 2020, and for whom a payroll submission has already been made to Revenue in the period from 1 February 2020 to 31 March 2020.

The amount employers can pay to their employees as part of this scheme has changed:

| 15 March 2020 to 25 March 2020 | €203 per week |

| 26 March 2020 to 3 May 2020 | Enter a non-taxable amount equal to 70% of the employee’s net weekly pay to: A maximum of €410 per week where the average net weekly pay is less than or equal to €586 or a maximum of €350 per week where the average net weekly pay is greater than €586 and less than or equal to €960. |

4 May 2020 to 31 August 2020 (Operational Phase) | In Phase 2, from 4 May to 31 August 2020, the scheme has proceeded to the operational phase, where the Subsidy paid to employers will be based on each individual employee’s Average Revenue Net Weekly Pay, subject to the maximum weekly tax-free amounts. |

| 1 September onwards | The Employment Wage Subsidy Scheme starts. For more information see The Employment Wage Subsidy Scheme |

Revenue has worked closely with DEASP to provide an option for employers to make this payment to their employees through the normal payroll process.

This means that employees can retain their link with their employers, allowing them to be paid a certain amount of money immediately.

The amounts paid to employees and notified to Revenue will then be transferred into the employer’s bank account by Revenue. This reimbursement will, in general, be made 2 working days after receipt of the payroll submission.

TIP: If one of your employees has been diagnosed with COVID-19, or has been told to self-isolate by a GP, then the employee can apply for illness benefit. Read more >

TIP: If one of your employees has been diagnosed with COVID-19, or has been told to self-isolate by a GP, then the employee can apply for illness benefit. Read more >

Inform your employees

If you've temporarily laid off staff as a result of the impact on your business due to the COVID-19 (Coronavirus) pandemic, you should advise your employees that you will be paying them this benefit.

Employees don't then need to register directly with the Department of Employment and Social affairs. If they've already registered directly, please refer to our FAQs guide.

Register with Revenue

TIP: The scheme closes for new applications from employers from 31 July 2020.

If you intend to participate in the Employer COVID-19 Refund Scheme, you must:

- Check the scheme applies to your business.

- Log on to ROS myEnquiries and select Employer COVID -19 Temporary Wage Subsidy.

- Read the declaration and click Submit.

- Log on to ROS and in Manage bank accounts, Manage EFT, ensure that the bank account details provided are correct.

Employers who have registered for the Emergency scheme or the Enhanced Payment scheme will also be required to register for the Wage Subsidy Scheme through ROS.

Download the CSV for the operational phase

From 4th May to 31 August, the maximum weekly wage subsidy amount payable to each employee has been calculated by the Revenue is available to download from your Revenue account as a CSV file.

The CSV file contains the Average Net Weekly Wage for each eligible employee on your payroll.

To download the file

- From within your Revenue account, go to the My Services tab.

- Within the Employer Services section, click Request RPNs.

- From the end of the page, click Request Temporary Wage Subsidy Scheme calculation, then Request Calculation.

- Enter your Revenue password, then click Sign & Submit.

The calculation CSV will then download.

NOTE: Note: You cannot import the CSV directly into Payroll.

NOTE: Note: You cannot import the CSV directly into Payroll.

Set up a Subsidy payment in Sage Payroll

The amounts paid to employees under the scheme are not subject to tax, USC or PRSI. You'll need to set up a special payment for employees under the scheme.

TIP: These payments should only be used for new transactions in Payroll. Retrospective business expenses do not need to be changed.

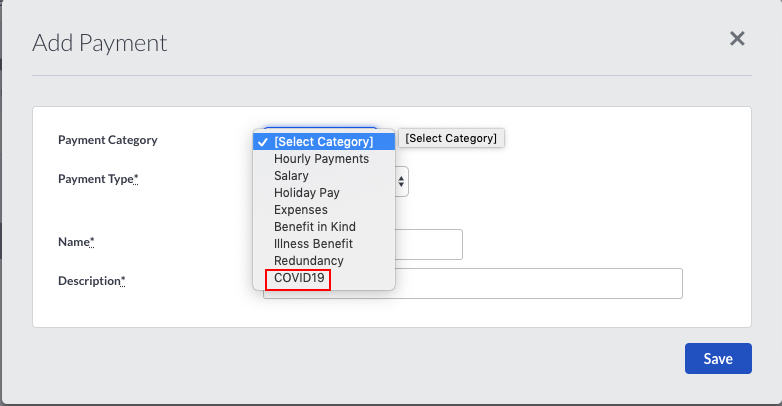

To create the COVID19 payment:

- From the Payments tab in Settings, select Create New Payment.

For the Payment Category, select COVID19.

This creates a payment which is not subject to PAYE, PRSI or USC.

- Click Save.

Process the payments

Edit your employee's PRSI codes

- From the Pay Runs tab, start the pay run you want to process.

- From the Edit Pay stage, click the employee name.

- Click the employee name that appears in blue. Change the employee's PRSI Code to J9.

Save your changes.

TIP: An alert message should appear to confirm the code is only for use when paying Covid-19 refund payments.

Record the payment

- From the Pay Runs tab, start the pay run you want to process.

From the Edit Pay stage, add a salary payment.

- If you are topping up your employee's salary, enter the top up amount here.

If you're only paying the Covid19 subsidy amount, create the salary payment for 1 cent. This is to trigger a payroll submission request.

Do not to include the Temporary Wage Subsidy payment in Gross Pay. If the subsidy figure is included in the gross pay, it will be treated as Additional Gross Pay. Revenue will apply tapering and your employer refund amount will be reduced accordingly.

Add a second payment for the employee using the Covid19 payment type for the amount you are paying them under the Wage Subsidy Scheme.

- From 4th May to 31 August, this is based on each individual employee’s average net weekly pay, subject to a maximum weekly tax-free amount. The amount payable for each employee can be downloaded as a CSV from the Revenue. See Temporary Wage Subsidy Scheme - Operational Stage

- From 19 April, this should be 70% of the employee's NET pay, up to a maximum of €410 Euros per week.

- If you're processing the payment for before 19 April, the payment is still 70% of the employee's NET pay. However, it's up to a maximum of €410 Euros per week where the average net weekly pay is less than or equal to €586 or a maximum of €350 per week where the average net weekly pay is greater than €586 and less than or equal to €960.

Check the PRSI insurable weeks

- Select the PRSI link in the deductions section. The number of insurable weeks should match the number of weeks your employee is being paid for.

- If the number of weeks is incorrect, select the Override standard insurable weeks check box.

- Enter the number of insurable weeks you wish to use for this pay run, then click Save.

Disclaimer

This article provides general rather than specific guidance to assist all of our customers. We always do our best to make sure that the information is correct but as it's general guidance, no guarantees can be made concerning its suitability for your particular needs. The information is valid at the time of publishing and is provided without any warranty of any kind, express or implied. You should take professional advice if you require specific guidance on your individual circumstances, for example to ensure that the results obtained from using our software comply with statutory or regulatory requirements. For Employers, PAYE, PRSI and general tax enquiries you should call Revenue of Ireland (ROS) National Employer Helpline on 01 738 36380 or visit their website at Revenue Online In no event will we be liable to you for any direct, indirect, consequential or incidental loss or damage arising out of or in connection with your use of the information provided.